Executive Summary

When considering energy security we should pay close attention to these main points:

- Energy systems are likely to be ~⅔ electricity and ~⅓ hydrogen and its products.

- Hydrogen uses include industry, synthetic fuels/chemicals, transportation; but domestic/commercial heating uses 6X as much energy as heat exchangers.

- Reliance on neighbours gives no energy security.

- By 2040, almost all European countries will depend on imported electricity during “times of system stress” (low renewable generation and/or high demand)

- Examples are after sunset on a windless winter evening, which can be extended by weather patterns to as long as a fortnight (kalte Dunkelflaute).

- These are largely concurrent, so if all are importing, who is exporting?

- Countries will not export if it means enduring black-outs.

- Resilience requires multiple, distributed, large energy hubs.

- Major interconnectors (gas and electricity) and energy hubs are vulnerable.

- However, no energy assets can power electricity grids at higher voltage.

- Therefore many of these hubs must be on the transmission grid.

- Gas grids need to be converted and extended for hydrogen.

- Conversion costs are affordable.

- Distribution, e.g. to remote industry and fuel stations, should be by pipe, hence a need to extend the grids; road and ship transportation is small and expensive.

- Enormous storage in salt caverns is needed, possible and affordable; and is minimised by synergies of co-location – but bearing in mind resilience issues.

- Electricity grids need reinforcing greatly.

- For electricity demand, transmission grids need to be more than tripled, and distribution grids even more.

- Grid reinforcement costs, in the UK, are £3bn per GW of new wind, increasing rapidly, just for the onshore part and excluding grid connection costs.

- To minimise grid reinforcement, renewables need to be connected to the grid through sufficient behind-the-meter large-scale long-duration electricity storage

- The electrification of heating, industry and transportation increase this need.

- Reinforcement needs are even greater to supply electrolysis, unless taken largely off-grid by co-location with renewables and suitable-scale storage.

- System Operation (non-energy grid running) costs also increase exponentially once renewable penetration passes 16% for systems with long-duration electricity storage at 5% of peak demand; lower thresholds if there is less storage.

- This can only be prevented if the majority of storage is naturally inertial.

- Storage must be at large scale and diverse durations: 4-8 hours, 8-12 hours, 12h – 3 weeks, seasonal and inter-year; types of storage vary according to duration.

- Zero-carbon power stations can reduce system costs and need for storage.

- Improving regulatory / contracting systems reduces the financial support needed.

- Storelectric’s technologies address almost every one of these issues in exceedingly efficient and cost-effective ways.

Energy Security Challenges

Events have shown that Europe needs to secure its energy supplies from external challenges and cut-offs. That much is well understood, proven by the 2022 energy shock and resultant desperate scramble for supplies of hydrocarbons. At the same time, investment in renewable energy was correctly (but largely ineffectively) targeted to wean the continent off dependency on imports.

Events in 2022 have also shown that each country must look after its own supplies:

- When French nuclear output was halved due to maintenance issues, the interconnector flows to the UK were reversed, causing shortages and price hikes in the UK;

- When Germany was short of gas, they cut their interconnectors even to EU neighbours to conserve supplies;

- Norway, one of the only European countries expecting to have exportable amounts of renewable electricity after 2040, passed legislation allowing them to cut their interconnectors during times of system stress.

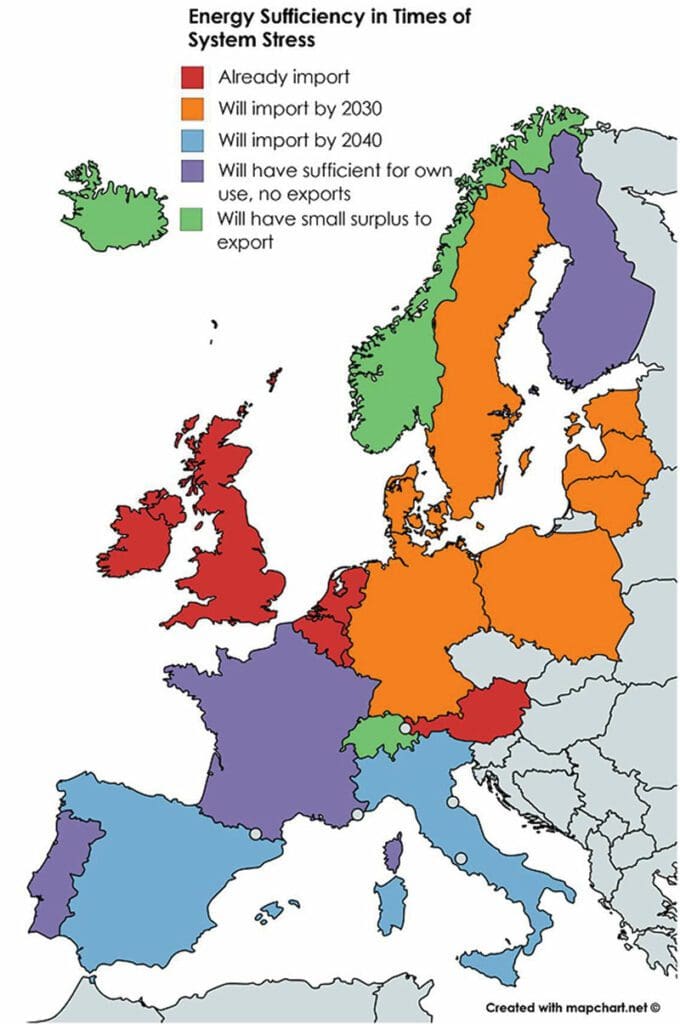

Indeed, the challenge of energy security is baked into the continent’s energy transition plans: by 2040 (based on 2019 plans of each country; the situation may have evolved since then) only three countries in Europe (France, Portugal, and Finland) planned to have exportable amounts of electricity during times of system stress. That was based on the assumption that France would build 40GW new nuclear on time and to cost; since then not a single nuclear power station has been completed. There are even questions about the energy self-sufficiency of Switzerland. Further analysis here.

A “time of system stress” is any period of high demand and/or low renewable generation, which occurs continent-wide after sunset on a windless winter evening, continuing at least until well after dawn; the kalte Dunkelflaute weather patterns can increase this to up to a fortnight. So if everyone is importing during such times, who is exporting? The results would be continent-wide shortages.

System Resilience

This is the primary challenge; the secondary challenge is the resilience of the system. As was shown by the sabotaging of NordStream 2, and threats to electricity interconnectors, reliance on a few major sources/lines of supply is not wise. The more distributed the supplies/supply routes, the more resilient the system will be. But this meets two different challenges:

- Economies of scale: distributed resources are intrinsically less efficient, cost-effective and capable (yes, even batteries are much less so than advertised);

- Providing transmission-scale energy: no grid has enough energy to power any higher-voltage level of grid, as proved by National Grid’s first engineering report in their Distributed ReStart project.

- Ignore the conclusions, and all subsequent conclusions, which all say that more work needs to be done; read the text, which says that it is both practically and even theoretically impossible.

Reliance on Neighbours?

The planning assumption throughout the European Union and the United Kingdom is that each can rely on imports during times of need, especially if contracts are in place. But contracts tend to be short-term, and Germany’s actions on gas show that even within the EU that principle cannot be relied upon. Indeed, which system operator would be prepared to tell their government that a black-out in a major city or industrial area was because they were exporting the energy needed, even if against existing contracts? As the Norwegian legislation has shown, even if this occurs once, it will be prevented from recurring.

Which Energy Systems?

The energy transition is essentially very simple, replacing coal and hydrocarbons with electricity, hydrogen and products of the two of them. This both focuses the thoughts of energy security on just two sectors, and helps greatly with energy security as they can be produced throughout the continent.

Very roughly, the 2010 energy system was ~25% electricity, ~25% liquid hydrocarbons and ~50% natural gas (coal is ignored, as that is mostly used for electricity generation). As electricity is much more efficient than hydrogen for many applications (e.g. light-use transportation, heat pumps which use 1/6 of the energy of heating with hydrogen), the 2050 energy system is likely to be ~⅔ electricity and ~⅓ hydrogen and its products; and the hydrogen will be mostly created by renewable electricity.

Although electric vehicles dominate clean transportation, by 2050 it is quite likely that ~⅔ of vehicles of all sizes (mainly the heavy duty ones – those used for long distances, large loads, frequent uses; also those without a personal electricity supply) will be hydrogen powered and account for ~90% of transportation energy use. Conversely, ~⅓ vehicles will be electric and account for 10% of transportation energy use. Further discussion is here.

Energy Security: Consequences for Gas Grids

The gas grid is relatively easy to convert. Most new and replacement pipes, for the last couple of decades, have been suitable for carrying hydrogen; their seals, pumps and ancillary equipment may yet need upgrading. Capacity-wise, the share of energy carried by gas may well reduce by ~⅓, which coincides with hydrogen’s energy density per unit volume as compared with methane; therefore the network does not need the radical expansion that the electricity grid requires.

What it will need is extension to new corners of each country as (for example) hydrogen is needed for distributed industry and fuel stations: only three tonnes of hydrogen can be carried by road tanker, and only expensive and highly energy-inefficient cryogenic cooling can put enough hydrogen into ships to be economic, making pipelines by far the best option for transportation.

Gas grids must also have lots of large-scale and long-duration storage for hydrogen, and the only cost-effective way currently available is salt caverns. Other geologies are difficult and comparatively costly, most of them impossible. Luckily, potential locations are plentiful throughout the continent. More details on hydrogen transportation and storage are here, together with how Storelectric offers them most cost-effectively.

The amount of gas grid and storage can be minimised by locating hydrogen-consuming industries with/near electrolysers. These should be powered by renewables, making their best locations by the cables of large renewable generation. However, hydrogen and hydrogen-consuming industries hate intermittency, which reduces their efficiency and plant life, and requires much more investment per unit output: even without considering the effects of intermittency, powering by 40% load factor offshore wind requires 2.5X as much plant per unit output as powering with baseload electricity; powering it by 17% load factor solar requires 6X as much.

Therefore large-scale long-duration storage should also be nearby, to remove the intermittency from the generation before it hits the electrolysers and other plant. And the more is co-located, the less energy storage and transportation is needed, as explained in more detail in a separate document together with indications of how massive savings and synergies can be achieved by such technologies (in which Storelectric leads) – with the slight caveat that enormous energy parks reduce resilience. Therefore such energy parks are best distributed around each country.

Energy Security: Consequences for Electricity Grids

Just to turn existing electricity grids renewable would, according to Breakthrough Energy, require increasing their size by about 3.5 times to accommodate the intermittency of generation and its balancing with storage and other means, which they deemed unaffordable even for America: if unaffordable for them, what hope do other countries have? This is confirmed by McKinsey: “The energy transition will require a dramatic increase in capital spending on the electric grid, delivered at an unprecedented pace.”

Yet that is only the start of the challenge. It ignored the costs of such balancing services, which would increase that figure greatly. Electricity will supply more needs than at present; according to the estimates above, rising from 25% of 2010 energy to ~67% of 2050 energy, maybe tripling the figure again. Hydrogen is created using electricity, increasing this total by another third. And all that is for the transmission grid: a massive roll-out of electricity consumption (e.g. for heat pumps and electric vehicles – another major reason why hydrogen has a big role in transportation) would require a comparable increase in distribution grids.

Based on public announcements and information from Ofgem and National Grid, the current cost of reinforcing the onshore UK grid (excluding the grid connection itself) is ~£3bn per GW of new offshore wind, rising exponentially; less than a year before, it was evaluated at £1.75bn/GW. Most of those grid increases can be saved by connecting renewables to the grid through behind-the-meter large-scale long-duration electricity storage of sufficient scale and duration, of which Storelectric’s are the most efficient and cost-effective.

The grid connection is halved for offshore wind, reduced by ~⅔ for onshore wind and ~5/6 for solar. Beyond the grid connection, output is according to demand, which the onshore grid is already built to supply: the reinforcements required are therefore reduced by much greater factors.

System operation costs (i.e. the non-energy costs of the grid) are also rising exponentially. In the UK (which had pumped hydro capacity of 5% of peak demand) that started when intermittent renewables accounted for ~16% of energy demand; if there is more naturally inertial large-scale long-duration electricity storage on the grid, the threshold rises; and vice versa if less. In the first three years from crossing that threshold, system operation costs escalated by over 14X or £8bn p.a. with no end in sight to that escalation. DC-connected systems, even with grid-forming inverters, cannot provide the same range of services – and cannot provide them concurrently with the same operational capacity, as naturally inertial AC-connected systems do.

If the behind-the-meter storage associated with renewable generation is naturally inertial, then the savings are greatly increased, and grid operation is vastly simplified: the combined renewables-and-storage could then be managed by the System Operator almost exactly as it manages power stations, delivering concurrently all the ancillary benefits too.

Issues of Scale

The challenges for energy storage are all at the grid scale and split naturally into groups of different durations:

- 4-8 hours (evening peak and overnight); CAES using salt caverns, pumped hydro.

- 8-12 hours (taking the intermittency from renewables); ditto.

- 12h – 3 weeks (weather periods extending times of system stress, to kalte Dunkelfaute two weeks plus any follow-on period before it’s replenished); CAES using porous rock geologies, and/or hydrogen generation.

- Seasonal (if we don’t have an ideal balance of solar and wind so month-on-month generation mirrors demand which, in the UK, is 1:5): hydrogen, or ~25% over-build of renewable generation against “contingency” or “reserve” contracts, or a combination of the two.

- Inter-year (energy incident on the planet can vary by 15% or more, over very long and irregular periods): ditto, but both would need increasing substantially.

Note that an over-build of renewables would not greatly help the first and third bullets, as there is little renewable generation during such periods.

Other Technologies

Other technologies can contribute to energy security, most notably nuclear. In any season, baseload demand is 40-60% of peak demand. Nuclear is best suited to delivering it: all variability is pure energy waste (like curtailment) and adds cost by consuming damping rods. As a rule of thumb, each GW of nuclear output (up to the limits of baseload demand) delivers the equivalent of 3GW offshore wind plus long-duration storage (8-12 hours duration or more), or 4-5GW onshore wind-plus-storage, or 6-10GW solar-plus-storage.

Biomass, biogas and similar generation also helps, but are severely curtailed in their prospects by the lack of feedstock without impacting global agricultural output or conservation areas. Some bio-energy with Carbon Capture and Storage (BECCS) will be necessary for negative emissions to counteract those of hard-to-abate industries, though the issues, costs and inefficiencies of CCS are rarely (if ever) considered completely in such proposals.

Financial Support, or Regulation?

If the right regulatory and contractual environment is in place to ensure energy security, no financial support is needed other than for first-of-a-kind plants, and maybe a few follow-on plants while a technology climbs down the maturity-cost curve; much of such support (certainly for first-of-a-kind plants at full commercial scale) should be in the proper domain of innovation funding, but tends to be excluded from such funding on the grounds that the plant would trade commercially, which is a large part of the reason why so many technologies are commercialised overseas.

The right regulatory and contractual support includes:

- Contracts of suitable durations (half of the amortisation life of the plant?) to provide returns for new build, with lead times to build them;

- Covering the quality of the outputs, not just its quantity;

- Contracts for reserve power/capacity; etc.

These are considered in other documents.